Asset location and asset allocation are two common themes in investing. Typically, someone who is younger is advised to have a more aggressive asset allocation (more stocks). Someone who is closer to retirement is often advised to have a more conservative allocation (more bonds).

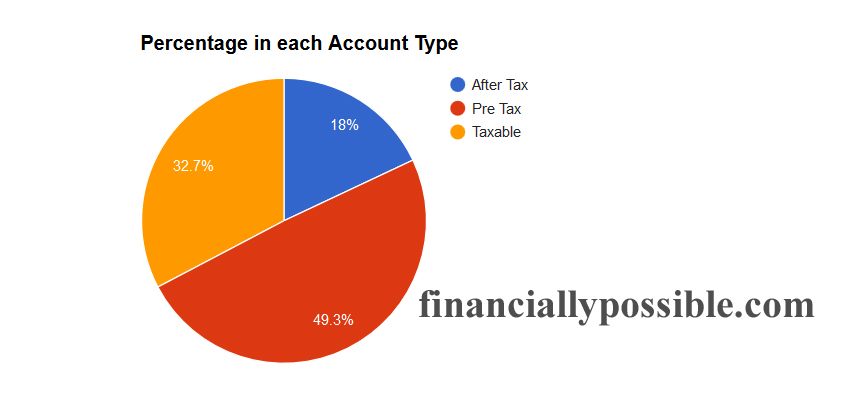

Where you choose to invest different asset types is intertwined with tax diversification. Having access to after tax accounts (Roth IRAs) is a key tool in lower your taxes on Social Security benefits in the future.

I began maxing 401K and Roth IRA accounts a few years after I started working, so taxable accounts are a larger percentage than I’d like. I would prefer that more of that money be invested into after-tax and pre-tax accounts instead.

There are some significant benefits to taxable accounts which are worth pointing out though. Anyone planning an early retirement needs taxable accounts until a Roth Conversion Ladder can be put into place (see also here). Also, taxable losses can only be claimed in a taxable account. This strategy is sometimes referred to as Tax Loss Harvesting.

Below is the percentage of my investment assets within each account type. Pre-tax refers to 401(k), 403(b), and traditional IRA (or SEP IRA) accounts. After-tax refers to Roth IRAs and a more recent after tax option available to a small percent of 401(k) plans participants.

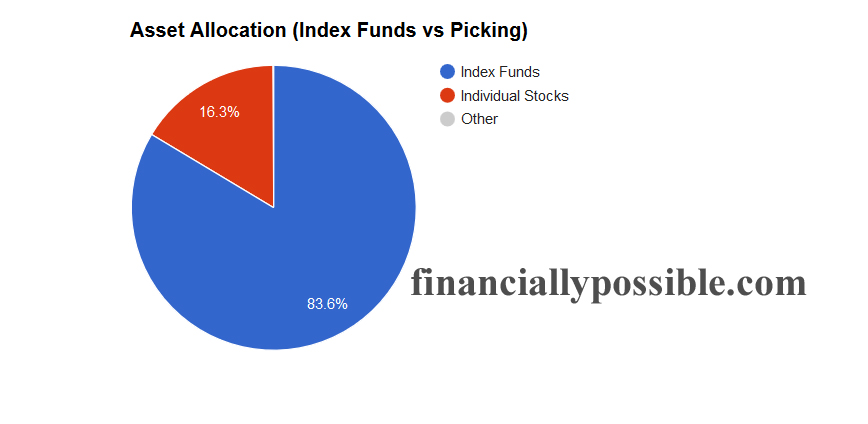

I am primarily an index fund investor. However, I have a higher percentage of individual stocks within my asset allocation than most investors who are part of the financial independence (FIRE) community. My paternal grandfather introduced me to the idea of selecting individual stocks.

**Disclaimer: This post contains affiliate links, which means that if you click on one of the product links and make a purchase, I”ll receive a small commission. Thank you for helping keep this site running.**

My investing knowledge and skills further expanded when a friend suggested I read Buffet: The Making of An American Capitalist. Nowadays, I don’t consider myself an expert investor, however, I feel very comfortable analyzing and evaluating a company’s financial numbers.

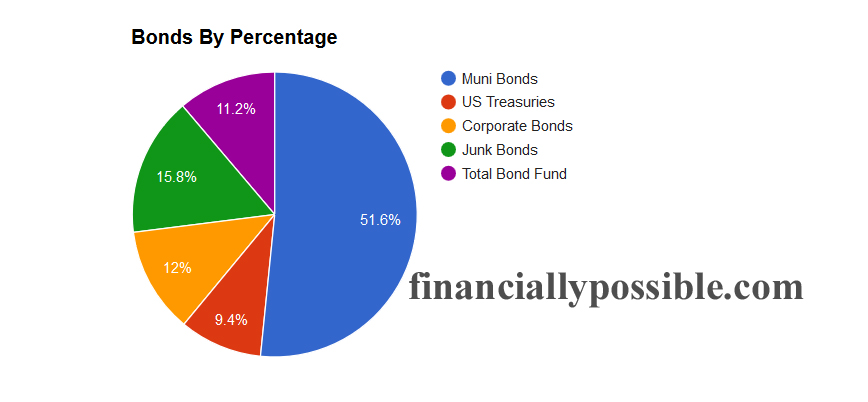

The chart below breaks down the different types of bonds in my asset allocation. Bonds currently make up 33.9% of the total. As you can see below, I am a fan of municipal bonds.

My maternal grandfather introduced me to this asset. He likes to buy individual municipal bonds. I am not that sophisticated yet. My bond holdings are in index funds. A recent post by Financial Samurai inspired me to learn more about purchasing individual bonds.

All my municipal bonds holdings are in taxable accounts, because these bonds are tax-exempt investments. The other types of bonds are held in 401(k) accounts and an IRA. Interest payments from these bond funds are sheltered from tax when held in these accounts. The interest payments also grow tax free.

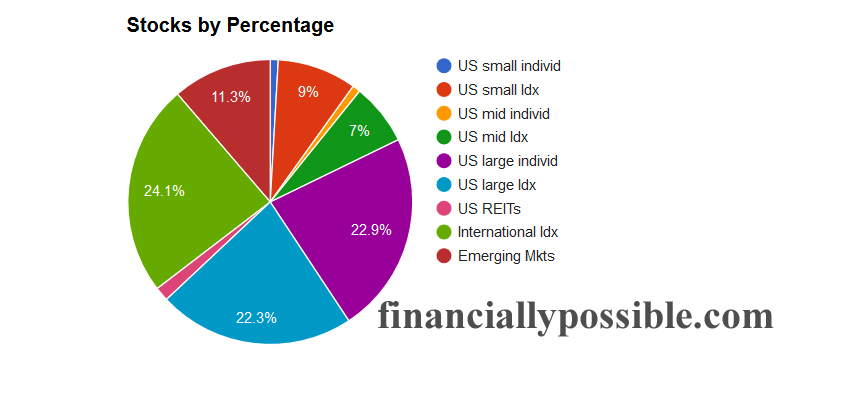

This next chart below breaks down the different types of stocks in my asset allocation.

Stocks currently make up 66% of the total. US large caps make up a larger portion of my holdings than those of small caps and mid caps combined. In terms of my non-US stocks, I favor developed markets over emerging markets.

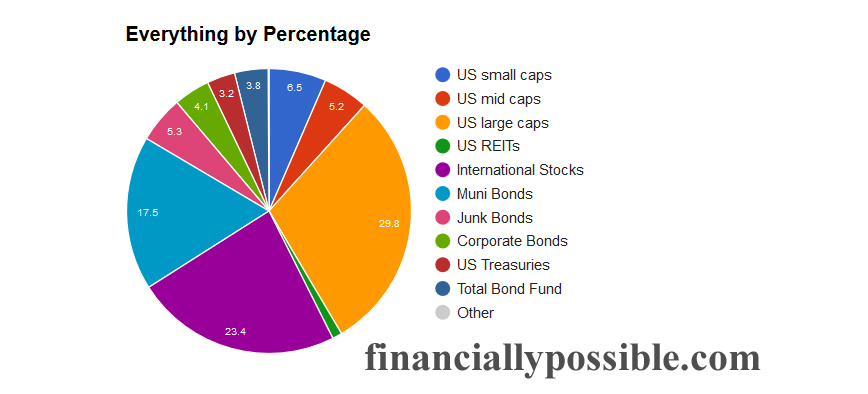

This last chart below shows my total asset allocation (which is the combined picture of the prior two charts). The first 4 categories (as shown in the legend) are US stocks (42.6%), followed by international stocks (23.4%). The subsequent 5 categories are bonds (33.9%). The ‘Other’ refers to cash which is a residual 0.1% resulting from dividends and interest payments. I periodically reinvest the cash.

As for asset location, most personal finance articles recommend holding higher yielding dividend stocks in pre-tax or after-tax accounts. This strategy shields tax consequences on dividend payments. For years, I wasn’t aware of this. Many of my higher yielding stocks are actually in taxable accounts. And because many of these holdings were purchased years ago when the prices were much lower, I’d have to pay heavy taxes on capital gains when I sell. That is, if I want to reinvest the money into a Roth using future contributions. If I were to go this route, I’d have to be very mindful of the wash rule.

Ms Financial Literacy and I plan our future contributions to our Roth IRAs to be index funds for US small and mid caps. Additionally, our ideal asset allocation is 45% US stocks, 25% international stocks, and 30% bonds. We’re using our current and future purchases through our 401(k) contributions to help get our investment mix back to our desired asset allocation. This type of strategy is rebalancing through future contributions rather than through multiple sell and buy actions.

For someone just starting out, I’d suggest a simpler model than how I’ve spread my investments. However, I provided my information as a reference point to get you reflecting about your own asset allocation and investment strategies.

What does your asset allocation look like?

How do you do your rebalancing across different account types and how often?