We have a lot to love about the month of February. There’s Valentine’s day, a holiday (President’s day) and celebration of black history. February is also the shortest month of the year. For those of us on salary (paid monthly or bi-monthly), we actually get paid more per diem this month than any other month! And if you’re into winter outdoor activities, February is a great time when you can go outdoors and build snowballs with kids.

The Purpose of Sharing Our Net Worth

In honor of Valentine’s day, I’m giving my readers and YouTube viewers a free gift by revealing my family’s net worth (me and Ms Financial Literacy). My goal is to show you what’s financially possible through the combined act of consistent high savings rate and diligent investing.

A secondary goal is to cut through the taboo of talking about money. I encourage you to be more open talking about money with others. There are so many positive benefits doing so, but I’ll leave that for a future post. At minimum though, talk about money with your spouse or significant other.

Scoreboard in Place of Net Worth

I do not love the term net worth. We all have much more to our worth that goes far beyond the amount of money we’ve managed to save at any given point in time. You have your skills, your relationships, friendships, health, and many other things of value. I prefer to think of net worth like a scoreboard. It’s simply a way to measure and keep track of where you’re at financially. From hereon, I use scoreboard in place of net worth.

February, being a winter month, naturally fits with the snowball analogy to building wealth. I described the similarities of building wealth and a snowball in a video format below:

During the past decade, my wife and I have been saving aggressively (between 55% to 70% of our net incomes), educating ourselves diligently on potential investments, and investing almost all of our savings. This combination of efforts has grown our snowball from a quarter million to 1.5 million, but the snowball is only possible for us because of a consistent high savings rate. Since I met Ms Financial Literacy, our annual spending has been anywhere from $25,000 to $50,000 which has always been far below our incomes. A move to another state greatly increased the cost of living, but also boosted our incomes.

You’re probably now thinking:

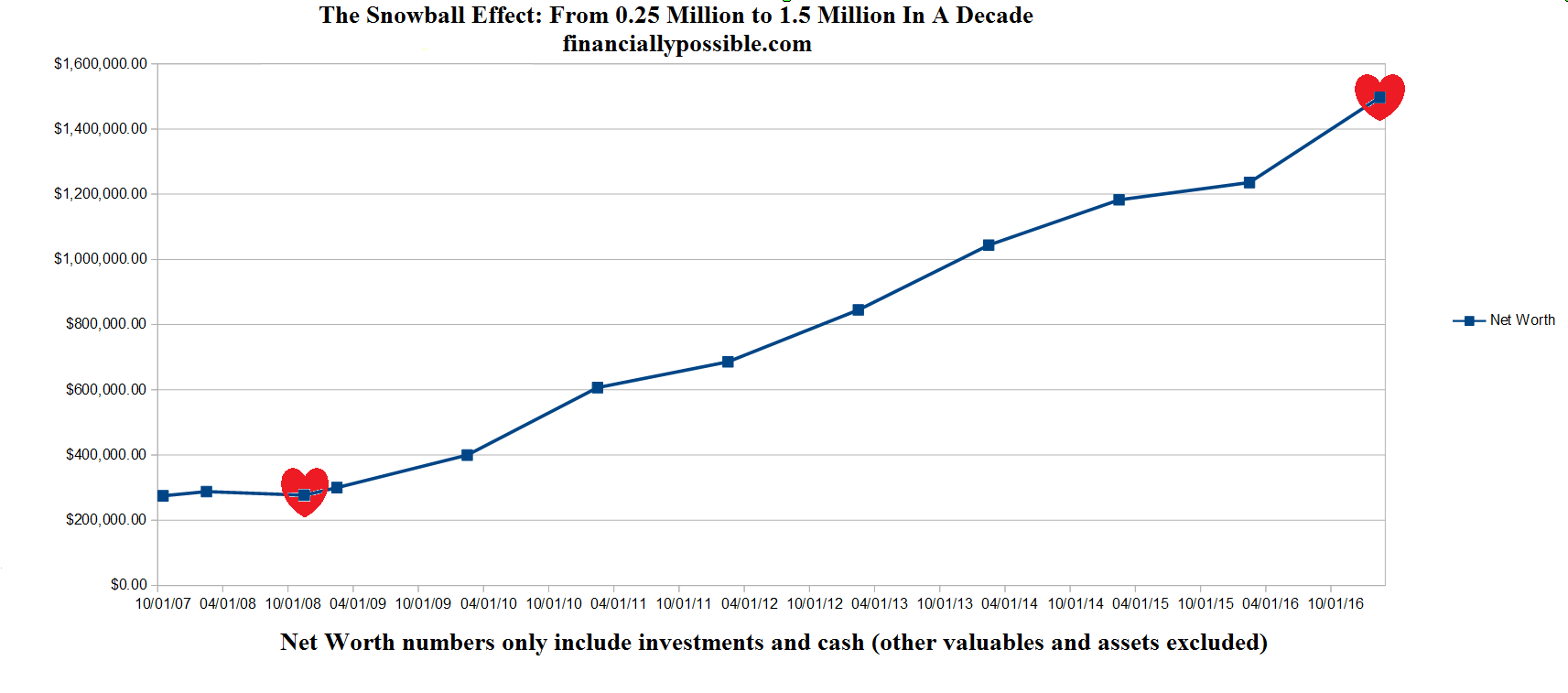

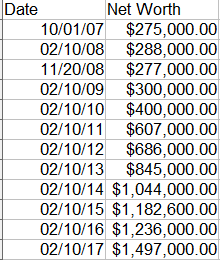

Ok, I feel you. But it’s only appropriate that I first describe the “how” before I show what my snowball looks like (click on image to enlarge):

The First Quarter Million

I have already worked for few years where the data tracking started. During those early working years I managed to save my first quarter million. However, I didn’t get excited learning about the stock market or investing until year 2007. For this reason, I do not have older data on my scoreboard as I did not track the scoreboard as closely back then.

Our Early Journey

The first heart on the graph is around the time when I met Ms Financial Literacy (I don’t have data on the exact date we met). She was a Ph.D student at the time and very frugal. Those were very memorable times for us. She was very excited to learn about investing. She began funding her Roth IRA even for tax year 2008 (you have until mid April in the following year to do so).

From October 2007 to February 2009, the scoreboard growth rate was fairly flat. As many of you probably recall, that was during the financial crisis of 2008 and 2009 (the financial crisis had two US stock market bottoms — November 2008 and early March 2009). Despite high levels of fear and chaos everywhere, I continued saving at a high rate during those times and invested in the stock market. This is why you’re seeing a fairly flat line rather than a big dip. In fact, I bought additional stocks aggressively during that time period and avoided selling any.

What followed after the financial crisis then has been a fairly smooth and steady climb. The money my wife and I continued to save got invested (i.e. packing on new snow) and we continued to accumulate more wealth through investment gains (i.e. the snowball picking up additional snow as it rolls downhill). And this pattern repeats through many cycles.

Our Recent Journey

By the end of 2014, we noticed we’ve reached a point where our annual investment gains were at or exceeding the amount of our annual savings. While this was very exciting for my wife and me, we did not use that event as an excuse to stop saving. In fact, we have almost completely avoided lifestyle inflation as our incomes continued to climb.

In the spring of 2016, we took a two-week vacation to southern France which was fairly expensive, but very worthwhile. We always enjoy travel and have traveled to many places, and Southern France has a special place in our hearts. The trip was worth every dollar (and even all the potential dollars we could’ve gained in future years from investments).

Year 2015 had the poorest annual return for stocks since the financial crisis. My graph makes 2015 look even worse. I pulled my scoreboard data from mid February of each year. The S&P 500 dropped 9.4% from January 1st 2016 to February 10th 2016. This causes the slope for 2015 on my graph to appear poorer than it would otherwise and the slope for 2016 to appear better than it would otherwise.

Let’s Grow Your Snowball

No matter what state your snowball is in now, I encourage you to grow your snowball. I’m confident you, too, can achieve a growth rate similar to my family’s if you:

- Consistently have a high savings rate (aim at 50% net each year).

- Educate yourself on investing: read books on investing and personal finance, read finance articles, watch my YouTube videos, connect with others who are good with money

- Invest diligently and avoid holding a large amount of cash.

Even if your snowball is in a very different place currently, you can still achieve a similar growth rate. You might need more time. The formula for getting out of debt and building your snowball is very similar; both start and end with living well below your means and having a high savings rate.

If you’re another financial blogger reading this and you’ve already got yourself a nice big snowball going (great for you!), then I still want to connect with you so we can bring about cultural changes in America. Money is the second most taboo topic (only telling other people how to raise their children exceeds it). Let’s work together to make talking about money less of a taboo topic.

What’s your next step for growing your snowball?

What would you tell your 18 year-old self about money?

What would you like to share with the community on what’s financially possible?

holy crap. how the hell did u have a 1/4 million 10 years ago? how old were u? whered that come from? i’m 34 and only have about 100k put away.

also, 600% return in 10 years is amazing haha. typical growth is typically means your money doubling every 10 years or so. obviously socking away so much money though is the main reason haha. you should easily have 3 million in 10 years, and 6 million in 20 years, even if you stopped saving totally.

i personally can’t save that much. i donate too much and have too many expensive hobbies (travel, photography, scuba diving) and i like to do it often. it’s hard to find a balance of having fun now and having fun later, and later isnt guaranteed. i could die tomorrow, so it’s very hard to determine your values. i guess everyone has their own line/standards. haha.

Hi Steve,

Sounds like your snowball is in great shape! You make a very valid point that not everyone wants to grow their snowball at the same rate. I’ve seen some of your photography; you’re skilled. Perhaps you can or already are using those skills to offset the cost of that hobby or even turn a profit. Have you heard of travel hacking and/or card churning?

I’ve always saved at a high rate of 50% or more which is how I saved the first quarter million. I also dislike debt (more on that here http://www.financiallypossible.com/my-biggest-financial-mistake-part-i/). I worked hard during high school to receive multiple scholarships in order to pay for my college. I came out of college debt free and with money in the bank due to working seasonally throughout college (every summer and even the winter breaks). There were also some years of work after college where I just wasn’t investing heavily in the stock market yet.

Money invested in October 2007 (when the market peaked) in a broad based S&P 500 fund would have only returned 89% to date. Not great for the time duration, but not bad either. I estimate that 60%-65% of the additions to our snowball was from savings. The rest was from market gains on the invested money with the money invested during the last half of 2008 and the first half of 2009 performing the best of course.

Your statement about reaching 3 and then 6 million assumes that either I and/or my wife keep getting an income to support our living expenses. While this may happen, it would only happen on our own terms. We’re choosing to buy back our own time and this may (or may not) involve taking some of the gains from the portfolio for our own expenses.

Very interesting and exciting. I will be following your future posts. I am fairly new to the investment game myself and am always looking to learn more about making my money work for me. Thank you for sharing about your personal experiences!

Hi Jeanine,

I’m happy to hear that you’re educating yourself on investing. We all start somewhere. I’m curious which books you have read or are you reading on investing and/or personal finance?

I speak about one of my first investments (and how poorly it performed) here:

https://www.youtube.com/watch?v=anE3TiWu7iY

Humans learn best from mistakes though.

Making your money work for you is so exciting. As I mentioned, in 2014 our annual investment gains began eclipsing our additional annual savings. It’s like having a whole other person (i.e. the money) working for you!

I love the snowball effect! Great job on building up your snowball to an avalanche. Having your money work so hard really gives you the freedom to pursue what you want, not what you have to do.